It was around 2 AM a few months ago when I decided to check my CIBIL score on a whim. Big mistake. I opened OneScore, ran the check, and my jaw literally dropped. 610. I sat there staring at the blue light of my phone in a pitch-black room, wondering how on earth things had gotten that bad. Then it hit me—an old consumer durable loan EMI for a TV that I mistakenly thought was on auto-debit, combined with a stubborn dispute over a Rs 1,500 broadband bill that I had refused to pay out of pure spite.

That petty spite cost me big time. A week later, I tried applying for a standard lounge-access card because I had a flight coming up. Rejected. Instantly. No human even looked at my application; the automated system just saw “610” and threw my request straight into the digital trash bin.

At first I thought, okay, let’s just try another bank. Maybe ICICI will be more forgiving than HDFC. Or maybe Axis will say yes. So, out of sheer panic, I went onto one of those big credit aggregator sites and spam-applied to four different cards within twenty minutes. I figured at least one of them would hit.

Honestly, this surprised me in the worst way possible: my score crashed by another 14 points within days. I didn’t know back then that every single formal credit card rejection triggers what lenders call a “hard inquiry.” To the banking algorithms, I suddenly looked like a desperate person starving for credit, which made them run even faster in the opposite direction. It was a massive learning moment for me. If your score is currently in the gutter, do not keep hitting the “Apply Now” button on random bank portals. You are just digging your own grave deeper.

Once I calmed down, I realized I needed a completely different strategy. I had to stop forcing my way through the front door and find a side entrance. Here is exactly how I managed to get approved for cards and rebuild my profile from scratch, without relying on luck or theoretical financial advice.

The Backup Plan: Fixed Deposit Cards

The absolute fastest, most foolproof way to get a credit card when your CIBIL score is completely ruined is the secured credit card route. I avoided this for a long time because it felt like a defeat. You essentially give the bank a fixed deposit (FD), and they hand you a plastic card with a credit limit that is usually 90% to 100% of that deposit amount.

At first, I thought, what’s the point of using my own money to get credit? But here is the secret: the bank doesn’t care about your awful credit history because they have your FD as collateral. If you run away or refuse to pay the bill, they will simply liquidate your deposit to cover the losses. Because there is zero risk for them, approval is practically guaranteed. But the magic happens behind the scenes—they still report your monthly payment habits to CIBIL. Every time you pay your statement on time, your score gets a little boost.

I spent days comparing these because I didn’t want to lock my money up in a useless account that offered zero rewards. I wanted something that actually gave me value while I fixed my credit mess.

I put together a quick breakdown of the three secured options I looked at closest when I was trying to figure out where to park my money.

FD-Backed Credit Cards Comparison

| Card Name | Cashback / Rewards | Joining Fee | Annual Fee | Reward Limits | Best Usage Category |

| IDFC FIRST WOW! | 4x Reward Points (No expiry) | Rs 0 | Rs 0 | No upper limit on earning | International spending & Fuel |

| OneCard (Secured) | 5x Rewards on top 2 categories | Rs 0 | Rs 0 | No caps on points | Local dining & Store offers |

| SBM Bank Paisa+ | 1.5% Cashback on online spends | Rs 0 | Rs 499 + taxes | Capped at Rs 1,000 per month | Online shopping |

I didn’t expect this, but the IDFC FIRST WOW! card ended up being a fantastic deal because it features a zero forex markup. I used it for a couple of online subscriptions billed in USD and saved a decent chunk of change. OneCard is also brilliant because their app interface is clean, and the metal card feel makes you forget you’re using a card backed by a meager Rs 10,000 deposit. The SBM Paisa+ card gives straightforward cashback, but that annual fee made me lean away since I was trying to save money.

Leveraging Co-Branded Shopping Cards

After about four months of religiously using my secured card and keeping my balances low, my score finally crept up into the late 600s. Still not pristine, but high enough to move away from purely secured options.

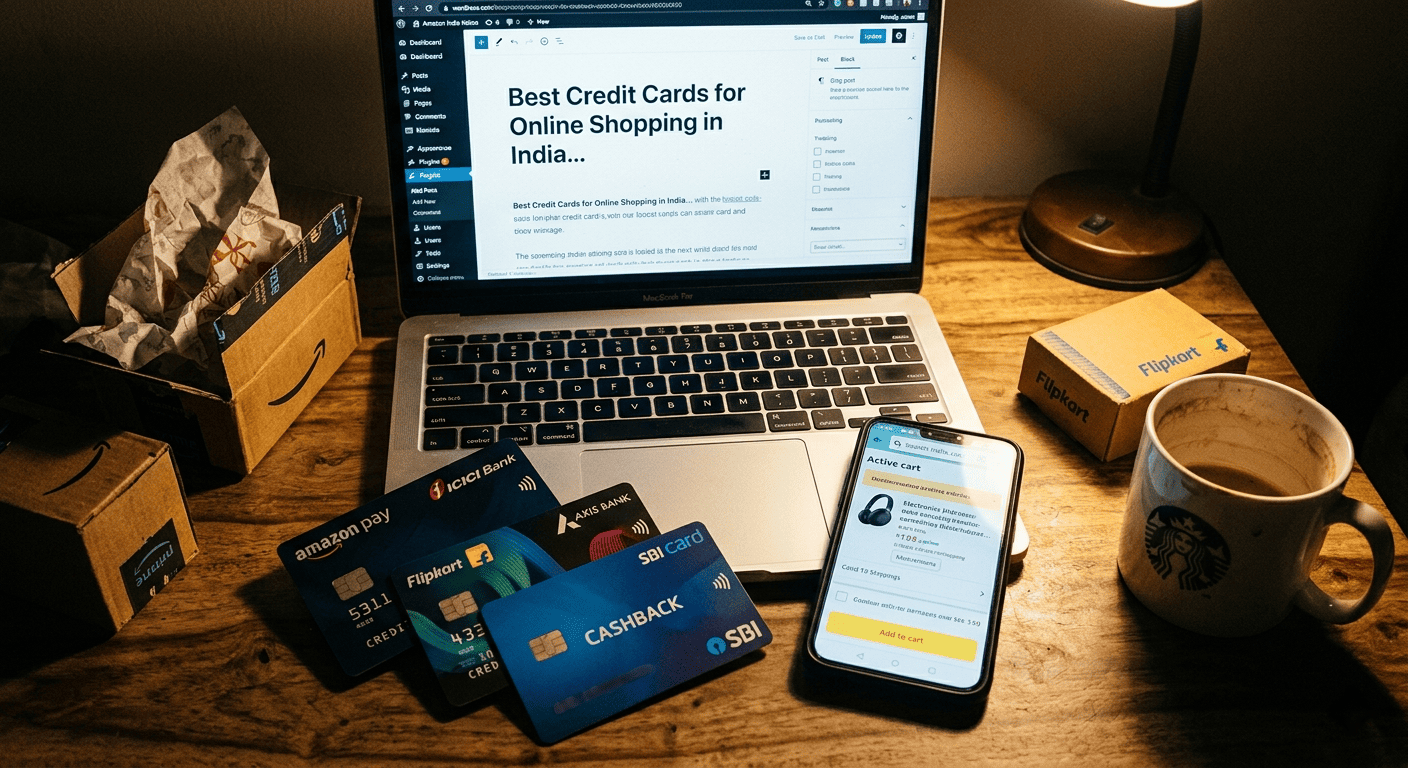

This is when I discovered the power of co-branded entry-level cards. Large banks love partnering with massive consumer tech platforms like Amazon, Flipkart, or Airtel. Why? Because these apps already track your real-world behavior. If you have been ordering groceries weekly on Flipkart or paying your utility bills through Amazon Pay for years, that data acts as an alternate trust signal. The bank’s risk engine looks at your account activity and realizes you aren’t a fraud risk, even if your CIBIL history has a few old scars.

I decided to try my luck with the Amazon Pay ICICI card because my primary shopping happens there. I didn’t apply through the bank’s portal; I applied directly through the banner inside the Amazon app.

This table shows how the top entry-level co-branded cards stack up against each other if you are trying to transition into unsecured credit.

Entry-Level Co-Branded Cards

| Card Name | Cashback / Rewards | Joining Fee | Annual Fee | Reward Limits | Best Usage Category |

| Amazon Pay ICICI | 5% for Prime users, 3% for others | Rs 0 | Rs 0 | Unlimited cashback | Amazon ecosystem shopping |

| Flipkart Axis Bank | 5% flat cashback on Flipkart | Rs 500 | Rs 500 (Waived at 2L spend) | Unlimited cashback | Flipkart & Myntra |

| Airtel Axis Bank | 25% on Airtel bills, 10% on utilities | Rs 500 | Rs 500 (Waived at 2L spend) | Capped per billing cycle | Monthly utility bill payments |

Honestly, this surprised me—the Amazon Pay ICICI card is completely lifetime free, meaning there is no pressure to hit a massive annual milestone just to waive a fee. It got approved for me with a modest Rs 30,000 limit, which felt like a massive victory after months of rejections. If you have high monthly phone, wifi, or electricity bills, the Airtel Axis card is a massive sleeper hit because that 25% cashback fills up your wallet quickly, though you do have to deal with monthly capping limits.

The Secret Weapon: RuPay Cards for UPI Transactions

If you are trying to repair your credit score right now, you have a massive advantage that wasn’t really a viable strategy a few years ago: linking RuPay credit cards to UPI apps.

CIBIL algorithms love activity, but they love consistent, clean repayment history even more. In the old days, you’d swipe your credit card maybe three or four times a month at a major retail store or a petrol pump. But with a secured or entry-level RuPay credit card, you can scan any local QR code at a tea stall, a grocery store, or an auto-rickshaw and pay using your credit line via GPay or PhonePe.

Instead of showing 2 or 3 transactions a month on your credit report, you are suddenly showing 30 or 40 small, successful transactions. You are building a massive mountain of positive payment data very quickly. I started paying for my daily morning coffee and casual snacks this way.

Let’s look at a few beginner-friendly RuPay options that are relatively easy to get or link against a small deposit.

RuPay Credit Cards for Quick Score Building

| Card Name | Cashback / Rewards | Joining Fee | Annual Fee | Reward Limits | Best Usage Category |

| Utkarsh SuperCard RuPay | 1% cashback on UPI payments | Rs 0 | Rs 0 | No major caps on base spend | Daily neighborhood UPI scans |

| IDFC FIRST EA₹N | Up to 1% back on UPI transactions | Rs 0 | Rs 499 | Capped via monthly point system | Small retail merchant payments |

| Suryoday Stable Money | 0.5% cashback + high FD interest | Rs 0 | Rs 0 | Standard rewards structure | Grocery runs & Savings growth |

The Utkarsh SuperCard is a great, low-profile option because it is completely lifetime free and gives you clean value back on everyday UPI scans. The Suryoday card is interesting because it works as a secured option but links you with high-yield fixed deposits, so your money isn’t just sitting idle making pennies while you fix your credit.

Using these cards for small amounts—like Rs 50 here, Rs 100 there—and clearing the total bill every single week kept my account looking incredibly healthy.

Real Hacks That Actually Moved the Needle

Outside of choosing the right cards, I had to change how I dealt with banks entirely. Here are the practical tweaks that actually got me results:

- The 30% Utilization Guardrail: If you get a secured card with a Rs 15,000 limit, do not go out and buy a phone worth Rs 14,000 on it. Even if you pay the entire bill the next day, the statement generation system will capture a high credit utilization ratio. This flags you as financially stressed. I kept my total active balance below Rs 4,500 at all times.

- The Mid-Month Payment Trick: I didn’t wait for the official bill to generate at the end of the month. I would log into my banking app every single Friday and clear whatever balance was outstanding. This ensured that whenever the bank reported my data to CIBIL, my utilization looked microscopic.

- Using My Salary Relationship: I stopped applying online blindly and went straight to the physical branch where my salary has been deposited for the past two years. I asked to speak directly with the branch manager. I showed them my consistent salary statements and said, “Look, my CIBIL is low because of an old utility dispute, but you can see my cash flow.” They have internal banking scores that can occasionally bypass automated CIBIL rejections for basic entry-level cards.

Fixing a damaged credit score feels like a slow, annoying process when you’re stuck in the middle of it. But the system is purely mathematical and highly predictable. Stop guessing, stop applying for premium cards you won’t get, stick to a basic secured card or a co-branded app card, use it for tiny UPI transactions, and let time do the heavy lifting for you.